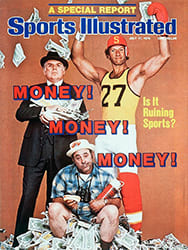

4 THE HIGH-PERCENTAGE SHOT

FACT: Pro teams are lucrative tax havens.

"It is almost impossible not to make money on a baseball club when you are buying it new because, unless you become inordinately successful, you pay no income tax," Bill Veeck confessed in The Hustler's Handbook, published in 1965. "It is, in fact, quite possible for a big league club to go on forever without ever paying any income tax.

"Look, we play The Star-Spangled Banner before every game. You want us to pay income taxes, too?"

Veeck should know. Early in his career, while studying accounting at night and dreaming up new ways to promote baseball by day, he hit on a wild idea. No, not the midget batter, but a gimmick of far greater consequence. Traditionally when an investor bought a team the players were considered part of the inventory, an existing asset like the shipping crates full of finished products in a widget company's warehouse.

Veeck's brainstorm was to buy the players' contracts in separate transactions and thereby make them a depreciable asset. The idea, which others later refined into an arcane science, was to arrange it so that the buyer could depreciate the cost of the players under the same tax laws and in the same manner that a farmer writes off his breeding cattle. After all, the theory goes, players depreciate in value—or get "used up"—just as aging bulls or creaky machines do.

When word of the Veeck variation swept through the offices of pro sports in the early 1960s, it was as if one of his exploding scoreboards had gone off in the accounting department. Some measure of the eventual impact of his idea can be gained from the fact that since 1959 football, baseball, basketball and hockey franchises have swelled from 42 to 101. A big reason for the increase was the desire of rich investors to take advantage of this sports tax shelter; no other industry in the land assigns a value to its employees and then writes them off as depreciable assets.

When an investor buys a team, he acquires two basic assets, player contracts and a bundle of monopoly rights called the franchise. The franchise is an intangible, non-depreciable asset; not only is its useful life span indeterminate but also its value, as we have seen, tends to accelerate. While that is another inspiring reason to leap into the sports business, the buyer cannot write off the non-depreciable cost of the franchise to reduce or "shelter" the income from his other businesses. For tax purposes, then, it is to the buyer's advantage to ascribe as small a portion of the purchase price as possible to the cost of the franchise. On many teams' books it is carried at a value of $50,000.

That done, the only things left for the buyer to do are to allocate the rest of the purchase price to the cost of the players and to decide how fast he wants to write that amount off—the span usually ranges from three to seven years. Until a recent revision in the tax laws set down more realistic but still generous guidelines, the buyer was encouraged to use his imagination. Example:

If an owner—let's call him Harry Hypothetical—bought his team for $10 million, allocated 75%, or $7.5 million, of the purchase price to the cost of the players and decided to depreciate them over the customary five years, he would have had a write-off of $1.5 million a year. If Harry was so inept or neglectful (he had other businesses to tend to, mind you, his real businesses) that the club showed an operating loss of $500,000 for its first season, for tax purposes the team's total loss would have been $2 million—the $500,000 operating loss plus the $1.5 million in player depreciation. If the team had been incorporated in a certain way (a tax device called a subchapter S corporation is favored) and if Harry, who was making a bundle in his other businesses, was in the 50% tax bracket, then he would have enjoyed a savings of $1 million—50% of the $2 million loss—on his income tax.

And so, after subtracting the out-of-pocket operating loss of $500,000 from the $1 million windfall resulting from player depreciation, there was Harry, decrying the perils of the sports business while palming a half-million-dollar profit. Even if the team had managed to earn an operating profit of $500,000, it still would have shown a book loss of $1 million. And Harry, though $1 million richer, would have been able to plead that, according to his tax records, the team was losing a bundle.

Harry's only problem was that he was being too cautious in assigning a mere 75% to player depreciation. In practice the percentages have been much higher. In 1966, when a group purchased the Milwaukee Braves for about $6.2 million and moved them to Atlanta, they wrote off 99%, which the IRS later brutally slashed to 91.7%.

Then there was the group that bought an NBA expansion franchise for $3 million and, moving in for a quick kill, wrote off 83% of the price on a fast-break schedule of just 18 months. As computed by Benjamin Okner, a government tax expert, this rapid depreciation of players, plus some modest tax advantages accrued from deferred player salaries and some non-cash team expenses, allowed the team to show a book loss of $1.6 million in its first season, while actually earning a $300,000 cash-flow profit. Okner concludes, "If the tax benefit to the owners from the $1.6 million book loss is calculated at a modest 50% tax rate, the $1.6 million loss is converted into a $1.1 million profit!"

And the player depreciation gambit is just for openers. When it came time for Harry Hypothetical to sell—and there was every inducement for him to do so once the depreciation cycle had expired—he could have cashed in on another tax break. As seller, Harry could have reversed the process, allocating 75% of the selling price to the franchise on the grounds that his astute managerial skills had enriched the team and caused its good-will value to soar. This maneuver would have allowed him to write off 75% of the profit from the sale as long-term capital gains, which would be taxed at a rate of about 30%. Meanwhile, the remainder, the suddenly diminished player contracts, would have been subject to something called depreciation recapture, meaning that it would have been taxed at ordinary income rates, which in Harry's case is 50%.

All told, Harry figured to have earned a return on investment that, depending on the sport, ranged from respectable to wow! If he had bought his team in the early boom period of 1962 and sold it in 1967, for example, economist James Quirk has estimated that Harry's rate of return would have been: baseball, 10.4%; basketball, 30.2%; football, 51.0%.

Following a study of pro basketball, economists Okner and Noll warned in 1972 of the "socially undesirable incentives for team owners. Except for a very few teams, the maximum profit a team could hope to earn is a few hundred thousand dollars. This is dwarfed by the tax avoidance made possible by depreciation. The gains to a rich individual or a corporation from owning a team depend very little on the quality of the team or its operations. In fact, among the most profitable teams are the lowly NBA expansion franchises. They field poor teams and do poorly at the gate, but the fast write-off of the expansion fee saves the owners half a million to a million dollars a year in income taxes. According to our conception of the public interest, society would be better served if the profitability of a team depended upon its ability to please the fans, not the tax accountant."

The obvious question about the sports tax shelter is: should public funds contribute to private profit? It is agreed that tax privileges are necessary to preserve pastimes that are of social benefit to a wide spectrum of citizens. Tax shelters are intended to encourage investment^ in high-risk ventures, the success of which is rewarding to the plungers and public alike. But how special should the tax treatment be—if special at all? When does encouragement to take a leap become license to hit and run?

Evidence indicates that minimizing financial risk maximizes another danger, that of attracting investors who are less interested in contributing to the development of their sport than they are in sheltering their income for a short while and then escaping with a profit. Indeed, the tax advantages tend to add to the value of franchises, thereby increasing the incentive for owners to get in early and get out quick. In fact, franchise values have soared so resolutely in the face of reported book losses that some cynics claim that they can foretell the day when an owner will decide to sell on the basis of his player-depreciation schedule and no other factor.

Dealings have reached that point in some basketball transactions. The 11 teams in the ABA experienced 27 changes of ownership in the league's 10-year history. Even the more established NBA has felt the impact of tax sheltering; between 1963 and 1975, the league had a turnover of 44 owners and principals. In many instances the owners seemed to be getting "used up" faster than the players they were depreciating. While old reliable John Havlicek pumped away like a well-oiled punch press through 16 seasons, eight different sets of Boston Celtic owners were writing him off for a total of more than $1 million in tax savings.

However, if some of the owners' maneuvers seem excessive, so too does the implication that vast numbers of teams have been snapped up in some kind of mad tax-haven boom. For one thing, the number of franchises with long-standing ownership militates against any easy generalizations about fast-buck artists. For another, many teams, particularly in the NFL, are too profitable in and of themselves to be subject to the whims of a quick-turnover market.

Still, the tax-shelter motive is there. It is strong and it has had a big impact on the course of the sports business. But critical to the shelter's future are reforms that evolved from a landmark tax case involving the Atlanta Falcons. When the Falcons joined the NFL in 1966, the owners allotted 91% of the $8.5-million entry fee to player costs. The IRS reduced that portion to 12%, thereby turning a book loss of more than a million dollars into a $1.2 million profit for the Falcons' first two seasons. Appealed and reappealed, the case was not resolved until early this year, when the Supreme Court upheld a ruling that had set the portion allowable for player costs at 38.8%.

Meanwhile, Congress passed the 1976 Tax Reform Act, which tightened the loophole with two half hitches. The act stipulates that the portion of the purchase price that the buyer allocates to player costs cannot exceed the portion allocated by the seller; there can be no more of what the IRS calls "whip-sawing." And it sets a limit on the allowance for player costs at 50%. Beyond that, the burden of proof is on the taxpayer.

While some owners fret that the tax reform might reduce franchise values by as much as one-third, that seems unlikely. There is still considerable room to maneuver under the new shelter—and in Congress, where the professional-sports lobby has been known to rush for a few first downs. Eagle President Jim Murray says, with a note of expectation, "The tax laws change more often than the standings."

But for now. Uncle Sam is only a half partner in the teams.

ILLUSTRATION

JOHN HUEHNERGARTH

Whoa, ol' pardner, here's a prime piece o' flesh ripe for a big of' write-off.