5 THE BUCK LATERAL SERIES

FACT: By one means or another, almost all professional franchises make money.

Heavy with gloom, Walter O'Malley once confessed at a baseball winter meeting that his Dodgers had lost $2 million that summer. His fellow owners were aghast. The Dodgers, one of the flushest franchises in sports, always made money. Only later was it learned that the Dodgers had actually netted $3 million but, according to O'Malley's arithmetic, that added up to a $2 million loss when compared to the $5 million they had made the year before.

While perhaps apocryphal, the story nonetheless illustrates how easy it is to play fast and loose with profit figures in pro sports. One reason for this is that owners, exposed as they are to a degree of publicity rare in other businesses, tend to move in mysterious ways, clasping their ledger books firmly to their breasts as they intone their favorite dirge, The Bottom-Line Blues. Their pose only serves to arouse suspicion. Alan Eagleson, director of the NHL Players Association, says, "NHL teams that make money won't open their books. You have no trouble seeing the books of those that lose money."

Ergo, the secretive owners are raking it in? Not necessarily, but certainly owners do not help their case by stoutly maintaining that their privately held businesses are just that—private—and that the profitability of their teams is not a matter for public scrutiny. Their detractors argue just as strenuously that, because the sports industry crosses into many areas of public policy and because it enjoys unique privileges under the tax and antitrust codes, the owners should be held accountable for their actions. For instance, should a profit-making enterprise operating in a stadium built with taxpayers' dollars be allowed to raise ticket prices indiscriminately or to pick up and leave town without justifying its financial need to do so?

Nevertheless, many owners continue to take the vow of poverty, regardless of how transparent it sometimes seems. Even within their own ranks, contradictions abound. San Diego Charger owner Eugene Klein claims, "Last year in the NFL we had eight to 10 teams that lost money." On the other hand, Oakland Raider Managing Partner Al Davis says, "Any dummy can make money operating a pro football club."

Bowie Kuhn, pleading in a 1976 Congressional hearing that baseball "is at best a break-even business," was asked why, then, the owners kept hanging in there. "Because they love the game and are willing to lose the money to stay in," Kuhn said. Hmm. A few months later, the top 24 players in baseball's first free-agent draft were signed for a total of $25 million. Then, after loud claims that the game would never again tolerate such extravagance, the first 14 players in the 1977 draft commanded $24 million. Where did all those break-even businesses get all that excess money? "The answer is obvious," says Marvin Miller, head of the baseball players' union. "They never were going broke."

In fact, Miller says that for the past 12 years, at the outset of each round of management-player negotiations, a representative of the owners has announced, "The clubs have not, do not and will not make any claim of financial difficulty." While this pronouncement runs counter to the poormouthing of management, it serves a very useful purpose: it effectively prevents the players from arguing that they should be allowed to inspect the owners' books.

The truth on profits lies elusively somewhere in between the usual claims of poverty by the owners and the assertions of the players that management is rolling in dough.

In 1971 the Brookings Institution brought together a team of financial experts to do the first serious study of the economics of the sports business. The experts' output, a technical 445-page book published in 1974 and entitled Government and the Sports Business, reaches several conclusions, not the least of which is that the sports owners are not at all receptive to having outsiders examine the financial facts. Though promised anonymity, a majority of the teams did not provide hard data, just as they have not for many congressional inquiries.

Economist Roger Noll, editor of the Brookings book, says, "If you were writing about the steel industry, you wouldn't have any trouble getting information. The professional sports industry is the most secretive business I know of."

Nonetheless, it is possible to make sound estimates about profitability without having access to all teams' books. The chart opposite shows the profit picture in the four major sports, but before reading it, remember that it indicates profit for the 1977 or 1977-78 season on only a cash-flow basis. As previously discussed, tax maneuvering can often make an apparently unprofitable team into a moneymaker. And as we shall soon see, there are other devices that allow owners to claim that they are losing money while actually turning a profit.

The publication of such unauthorized profit-loss data makes the owners very testy, and they choose to dismiss nosy economists as number pushers who are so dependent on figures that they have no grasp of the intangibles of the sports business. But the truth is that the owners themselves hardly lack for figures; in fact, most teams, like a lot of businesses, keep two sets of books, one for tax purposes and one to keep track of what is really going on. One version bears about as much resemblance to the other as Winnie-the-Pooh does to War and Peace. And accounting methods vary widely, sometimes leaning more heavily on the stubby pencil than on the computer readout. "We're not as efficient as we should be," says Patriot owner Billy Sullivan. "Football really isn't run like most businesses. Budgets are never done. Expense accounts are kept on the backs of envelopes. We don't set goals."

One result is what Noll calls "this magical and mystical problem." After studying teams' balance sheets as a witness for the government in tax cases, Noll says that the publicly held franchises and joint stock corporations that publish financial reports and are required to follow fairly rigorous accounting procedures "show different numbers, on average" from privately held clubs.

"The Seattle SuperSonics and Milwaukee Bucks are normal corporations traded in the stock market," he says. "Almost every year they make a profit. Yet, if you look, on average, at professional basketball teams they all seem to be losing money. Seattle and Milwaukee are not big cities. They shouldn't be atypically profitable in that league, but nevertheless they appear to be from looking at the books. So, I don't have a whole lot of confidence in the information I have seen."

Another skeptic is Joe Hamper, who is a vice-president of the Baltimore Orioles. He says, "There are no requirements from the league to have the statements audited. People seem to be hung up on secrecy. Some clubs are making a heck of a lot of money, and they could be embarrassed by the press. There are a lot of little games that people play."

One of them might be called the G&A gambit. Though the players' unions may claim otherwise, G&A does not stand for greed and avarice, but for general and administrative costs, a balance-sheet category that includes the salaries of management. Some owners pay themselves a wage that just as easily could be called a profit. That is, a privately owned team that breaks even and pays its owner $100,000 is no different from one that shows a $100,000 profit and pays its owner no salary. Economists note that a team's G&A totals tend to rise and fall with its fortunes, suggesting that some owners award themselves higher salaries in flush years.

G&A is also the catchall for expense accounts. When a minor partner sued Philadelphia Eagle owner Leonard Tose last year for "extravagant and wasteful" spending, the plaintiff alleged that the flamboyant trucking magnate had charged the club more than $20,000 for trips to Las Vegas and other U.S. cities and to Acapulco, $9,120 for his personal helicopter, $2,000 for 16 season tickets for his daughter, and took about $200,000 a year in salary and other expenses. Tose, who paid no personal income tax the first two years he owned the Eagles, countersued, calling his partner's action "contemptible."

Shortly thereafter, the First Pennsylvania Bank, which had loaned Tose $10.5 million of the team's $16,155,000 purchase price, sought to foreclose, noting that, despite a near-sellout season and $2.3 million in broadcasting revenues, the Eagles had reported a $1.2 million loss for 1976. By comparison, the Green Bay Packers, who have some 10,000 fewer seats and are the NFL's only publicly held team, reported a $455,000 profit that year.

Other variables that blur the profit picture are the roundabout ways by which many owners collect their money. Some make loans to a corporation that they set up to buy the team. That allows them to take their profits in the form of interest on the loan, which will then show up on the team's books as a tax-deductible expense. Other owners, doubling as landlords, reduce their teams' profitability by charging them abnormally high rents. For example, according to Noll, the New York Knicks and Rangers, both subsidiaries of the Madison Square Garden Corp., and the Boston Bruins, owned by the Boston Garden and Arena Corp., have paid rents that were about double the going rate.

Thus, Noll reported in the Brookings study, "The profits of the Knicks, including the amounts finally attributed to the team's parent corporation through rent and concession income, are at least $2.5 million annually, and perhaps substantially more."

As a result, when an owner can take a financially robust team and apparently reduce its health, first by taking player depreciation and then by draining off indirect profits—owner salaries, expense accounts, interest payments and high rents—the anemic balance sheet that often results is a distortion of the real profit picture.

Certainly owners not only have the right but also the duty to minimize their tax liabilities any way they can under the law. However, the attempt to evoke public sympathy by passing off the rack of bones that survives after player depreciation and other bookkeeping ploys have been computed into a team's balance sheet as an accurate portrait of the club is, at best, a questionable practice.

A Noll study in the Proceedings of the Conference on the Economics of Professional Sport also analyzed a sampling of balance sheets and estimated that, with player depreciation, interest payments and other hidden returns to owners figured in, the earnings of pro basketball were $20 million higher than the teams' ledgers seemed to indicate. The report estimated that NBA clubs made some $7 million, instead of losing $13.5 million as the owners claimed. The report also computed the profitability of an average team in each of the four major pro sports for various years. Though dated, the results reflected in the table above give an indication of what a team's profits can look like before and after tax writeoffs are figured in.

One reason there is no variance between the NHL's pretax profits and its benefit of ownership is that three of the wealthiest franchises are located in Canada, where the tax laws do not permit player depreciation. "They kick the hell out of us up here," says Harold Ballard, owner of the Toronto Maple Leafs. With the $1.1-million profit shown in the NFL, it was little wonder that 22 groups vied for the Tampa Bay and Seattle expansion franchises. Or that the winner in Tampa Bay, Hugh F. Culverhouse, is a noted tax lawyer.

NFL earnings, thanks to a hefty national TV contract, have most certainly risen since the Noll study—F.A.N.S. projects an average pretax profit of $3.9 million per NFL team for 1978—as have the fortunes of baseball, in which 15 teams reportedly made record profits last season. NBA earnings have undoubtedly increased since the merger with the ABA, while the profit picture in the NHL, which lacks both a network-TV contract and a merger with the WHA, has probably darkened considerably for some teams. The WHA is still in trouble.

A sampling of 1977 or, in basketball, 1976-77 profits from random teams:

[originallink:10598046:70789]

All things considered, the vast majority of teams are profitable, going concerns, but none is likely to produce any budding Onassises.

So to return to the burning question: are the owners really going broke? The answer is no. On the other hand, did anyone ever really believe that they were? Score another no. Now if only the owners would address themselves to another question: should they continue the poor-mouthing? Again, someday, maybe another no.

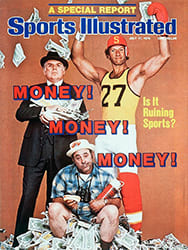

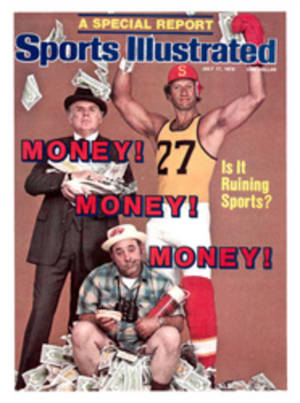

ILLUSTRATION

MICHAEL RAMUS

Owners are skilled at milking their teams for the so-called "benefits of ownership."

CHART